Expedia Spin-Off Creates Immediate Buying Opportunity

Expedia Inc. (EXPE) is spinning off subsidiary TripAdvisor. The TripAdvisor spin off will include TripAdvisor Media Group which is the world’s largest travel site. I believe the spin off will provide a catalyst to a higher Expedia share price. In this article I will discuss the spin off catalyst so investors on the sidelines can consider buying Expedia shares.

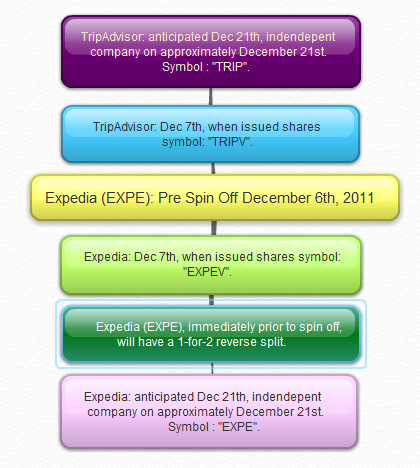

Expedia has provided investors, in my personal 'snap shot' view below, what the company looks like now and what the company will look like intwo weeks:

Expedia Background

Expedia is a leading global online travel company. Expedia's brands provide synergies to provide low cost travel services to businesses and consumers. The company offers hotel rooms, car rentals, airline tickets, and complete vacation packages. The company’s brands include Expedia web sites, Hotwire.com, Classic Vacations, Egencia, TripAdvisor, eLong, Venere NetSpA, and Hotels.com. The brand eLong is China's second largest travel booking site. Classic Vacations provides luxurious travel accommodations. Hotwire.com provides discount travel accommodations within the United States.

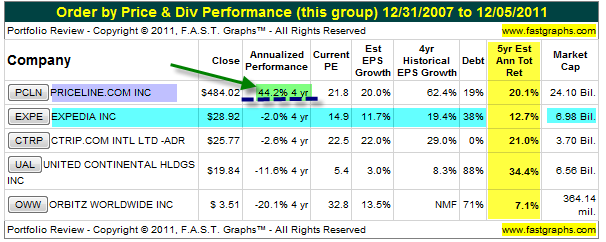

Priceline.com Incorporated (PCLN) is a competitor to Expedia and TripAdvisor. Priceline.com is an online travel company that offers airline tickets, hotel rooms, car rentals, and vacation packages. The company is well known for their "name your own price" service. This service allows potential customers to bid their maximum price for travel accommodations. Many consumers are aware of Priceline due to William Shatner's commercials over the years. Mr. Shatner has become a billionaire due to the Priceline stock appreciation.

Orbitz Worldwide, Inc. (OWW) is a competitor to Expedia and TripAdvisor. Orbitz is a smaller enterprise with a market value of $350 million. The travel industry operator's size does matter because of the ability to agree upon favorable terms with third parties. Orbitz allows businesses and consumers to research and book travel accommodations. Brands include Orbitz, CheapTickets, ebookers, RatesToGo, and HotelClub.

Ctrip.com International Ltd. (CTRP) is in prime real estate when it pertains to travel planning. The Chinese business has a balance sheet with zero debt and a market cap of $5 billion. The company offers travel packages, travel planning, and travel services within the People’s Republic of China. Priceline, Orbitz, Expedia, and TripAdvisor all desire growth in the Chinese travel industry. Ctrip.com assists consumers with booking and purchasing domestic and international flights from China.

Insider Ownership

Barry Diller, Expedia’s Executive Chairman, owns 27.2% of Expedia common “A” shares and 100% of Expedia Class “B” shares. The “B” shares are equal to 10x an “A” share in terms of corporate governance voting power. Liberty Media owns 24% of Expedia shares.

Expedia’s capital share structure includes 274,255,669 common “A” shares. In addition, the company has 25,599,998 Class “B” shares.

Institutional ownership is strong with T. Rowe Price owning 14% of Expedia shares.

TripAdvisor Background

TripAdvisor's travel research platform consolidates traveler reviews and opinions. The reviews and opinions pertain to visited global destinations, accommodation experiences, and restaurant insights.

2010 Earnings and Revenue

TripAdvisor, separated from Expedia, in 2010 earned $261 million in earnings before interest, taxes, depreciation and amortization ((EBITDA)). TripAdvisor's 2010 revenue was $485 million.

Current Expedia Valuation

The reason I recommend buying Expedia shares is due to the actual growth and the future growth prospects. In 2011, the Expedia should earn approximately $1.75 per share in 2011. Earnings estimates for 2012 are approximately $2.15 per share. This represents a 22.8% anticipated earnings per share growth rate. Expedia is currently trading at a 16.7x price to earnings multiple. Expedia, for 2012’s $2.15 earnings per share expectations, is trading at a 13.59x price to earnings multiple. The 13.59x is low considering a projected 22.8% growth rate in 2012 earnings per share.

The company is aggressive in buying back shares. In 2005, Expedia had about 348 million shares outstanding. In 2011, Expedia's share buy backs reduced this number to 270 million shares. The fewer number of shares outstanding, the higher the earnings per share everything being equal.

The company continues to sign 3rd party partnership agreements to enhance revenues and earnings for future years. The two separate companies can thrive on their unique business models.

Expedia, on December 6th, signed a new agreement with United Continental Holdings, Inc. (UAL). United Continental and Expedia have worked together for almost 15 years. Expedia and Hotwire will have access to all United and Continental fares, and schedules for booking flights.

Expedia began a 7 cent per share quarterly dividend during the 1st quarter of 2010. This equates to a 28 cent annual dividend. This amount is likely to increase in future quarters. The yield right now is less than 1%, but the catalyst for the spin off should awaken shareholders to the growth potential of each unique company.

Spin Off Terms

The Expedia spin off will result in two publicly traded companies. The first is Expedia, which will retain domestic and international operations of travel transaction brands including Expedia.com, Hotels.com, eLong, Hotwire, Egencia, Expedia Affiliate Network, CruiseShipCenters, Venere, Classic Vacations and carrentals.com.

The second company is TripAdvisor. TripAdvisor assets include thedomestic and international operations associated with the TripAdvisor Media Group, which includes its flagship brand as well as 18 other travel media brands.

Summary

The Expedia spin off of TripAdvisor Media has the potential to unleash a significant growth story. Travelers are increasingly shopping online for the best travel packages. Expedia and TripAdvisor both play a key role in providing a positive and inexpensive traveling consumer experience. The potential for increased mobile travel purchases is in its infancy. The potential for increased travel to China, India, and Latin America is increasing ever year.

TripAdvisor’s growth strategy is impressive. Per the November 25th road show presentation, TripAdvisor is actively growing in China. A growth initiative via the mobile platform is gaining increasing traction. The company has significant market share presence and visitors to its web sites.

The current Expedia is trading at a very low valuation. For the almost complete 2011 fiscal year, Expedia is trading at a 13.59x price to earnings ratio. The company is anticipated to grow earnings at 22.8% for 2012. The company's stock price is dislocated from projected 2012 earnings per share multiples.

Disclosure: I am long EXPE.